Malaysia's General Insurance Industry Posts 4.0% Growth

Kuala Lumpur, 8 October 2025 – Malaysia’s general insurance industry recorded Gross Written Premium (GWP) of RM12.3 billion in the first half of 2025 (1H2025), marking a 4.0% increase from RM11.8 billion recorded in 1H2024. This GWP growth is underpinned by strengthened operational performance and improved efficiency across the sector with underwriting profit results improving by RM153 million to RM629 million.

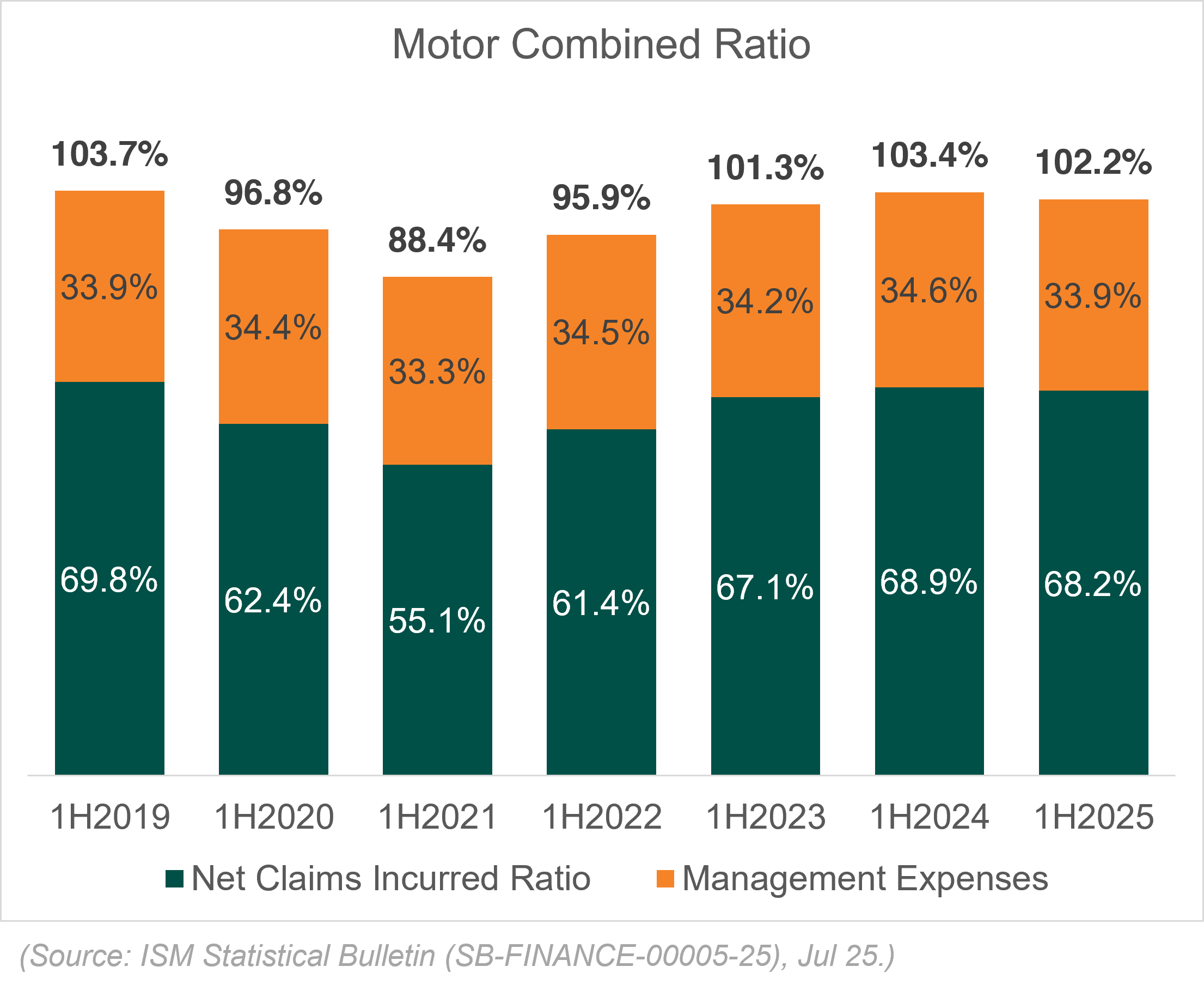

Motor insurance, which remains the industry’s largest line of business at 42.8% of total premiums, continued to register underwriting losses with a Combined Ratio of 102.2%. The underwriting loss was mainly due to higher claims ratio and claims frequency.

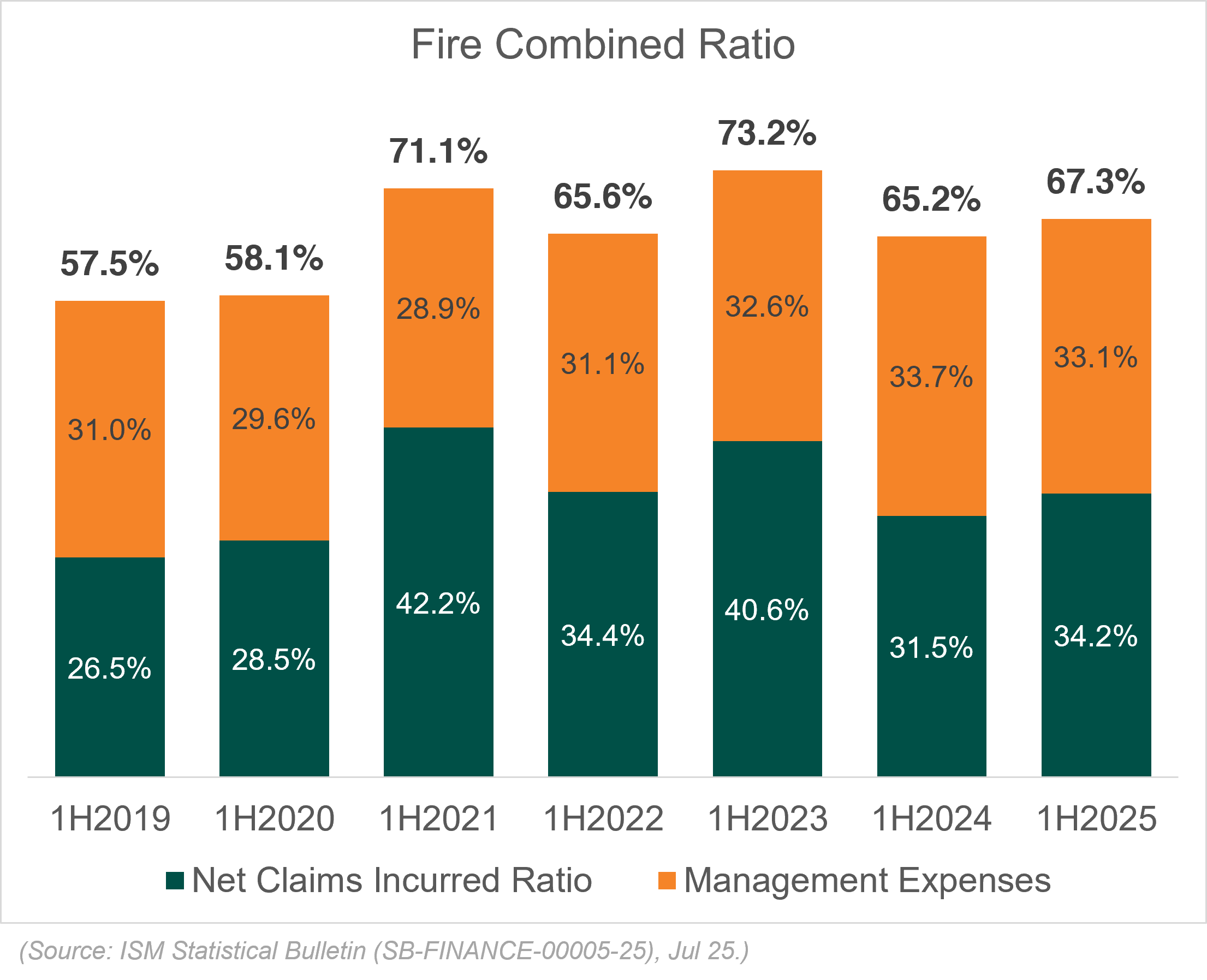

Non-motor business lines particularly Fire, Personal Accident (PA), and Marine, Aviation & Transit (MAT), contributed positively to the overall underwriting result. Fire insurance recorded a Combined Ratio of 67.3%, while MAT and CARE segments also remained profitable.

Motor and Fire Lines Continue to Support Industry’s Performance

The combined performance of Motor, Fire and PA insurance collectively contributed to 5.6% growth in GWP for the general insurance industry in 1H2025:

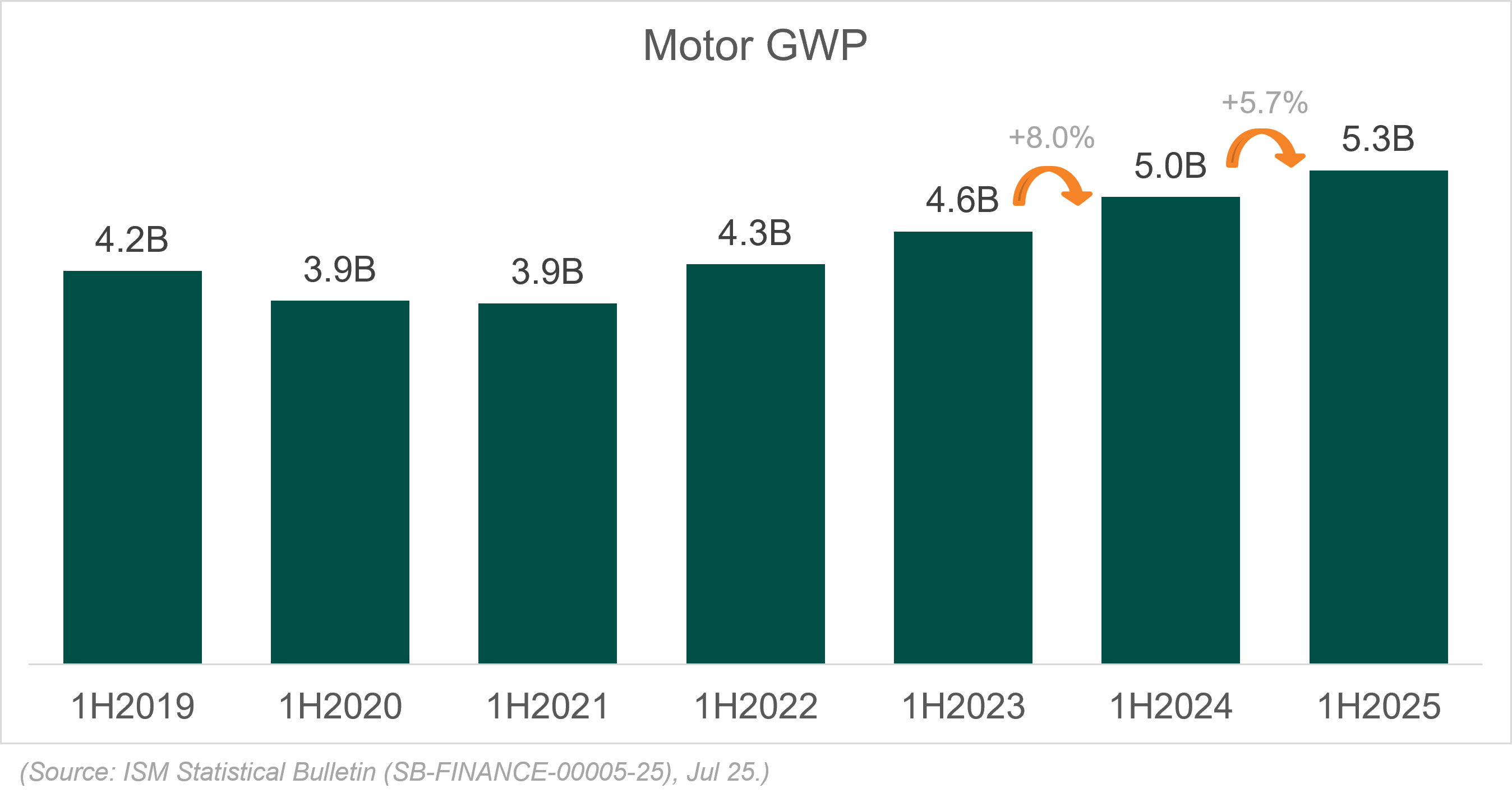

- Motor insurance remained the industry’s largest business line, contributing RM5.3 billion and representing 42.8% of the portfolio. The Motor line recorded a slower growth of 5.7% YoY in 1H2025 versus 8% in 1H2024.

- Fire insurance showed stronger performance and is the industry’s second largest business line, contributing RM2.6 billion and representing 21.1% of the portfolio. The Fire line growth hovered around 10.4% since Q42024.

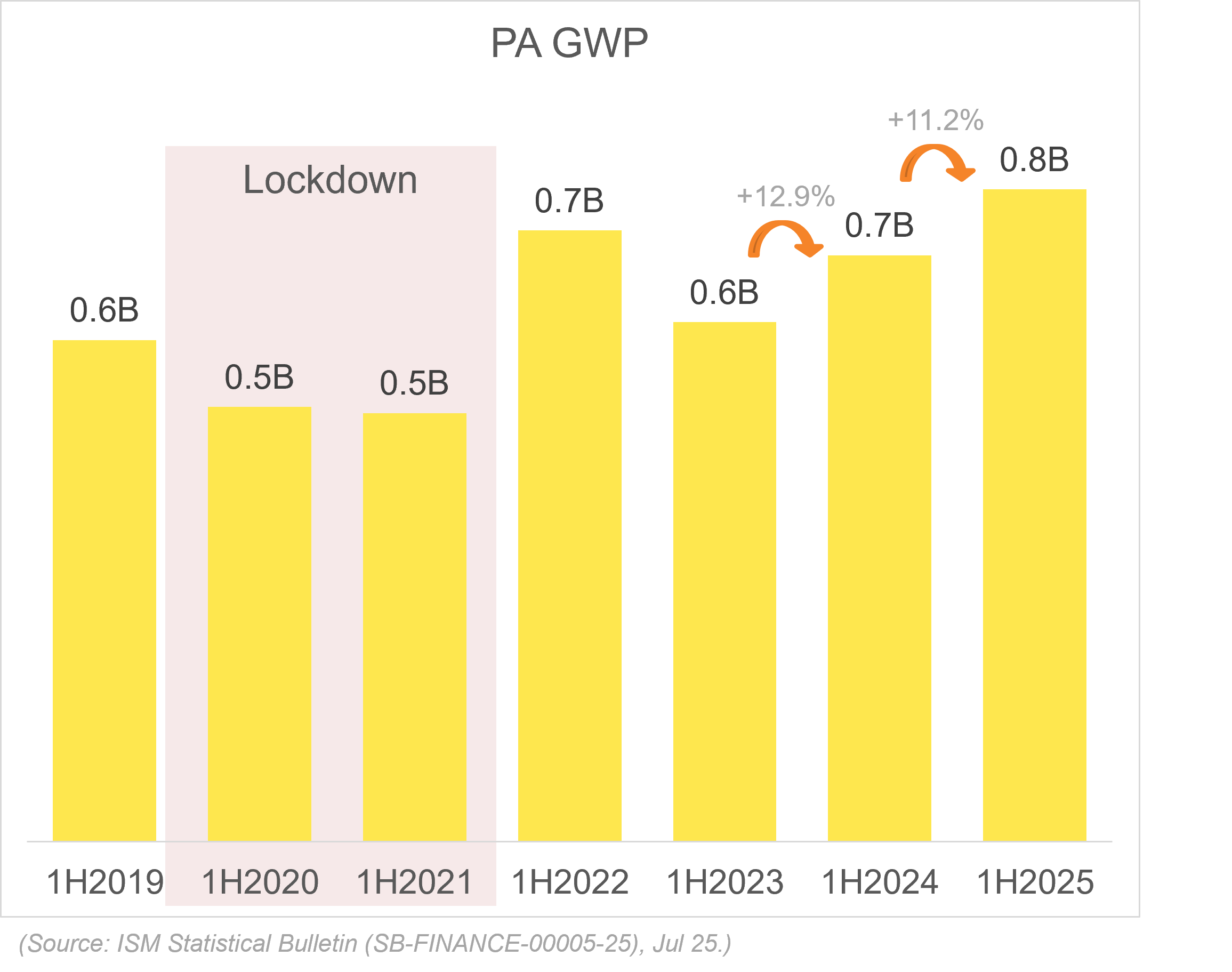

- PA, a growing segment, reached RM0.8 billion in 1H2025 with a 11.2% growth rate. This line of business represents 6.4% of the portfolio

Motor insurance

Motor insurance continues to operate at an underwriting loss, recording a Combined Ratio of 102.2%, a reduction of 1.2 points from 1H2024, due to a slight improvement of claims ratio from Motorcycle and Commercial Vehicle segments. This underscores the ongoing need for disciplined underwriting and efficient claims management, a necessity driven by persistent sector-wide challenges:

- Rising claims frequency: Number of road accidents in Malaysia consistently trending upward to 115 cases per 100,000 population since 2022.

- Spare Parts Inflation: The average parts price increased with a Compound Annual Growth of 10%, driven by heavy reliance on imported components for newer vehicle models since 2021.

Chart of GI Motor GWP Trend

Chart of GI Motor Combined Ratio Trend

Fire Insurance

Fire insurance grew by 10.4% from RM2.3 billion to RM2.6 billion in GWP, supported by infrastructure-led commercial property growth and ongoing demand for real estate protection. The segment reported a Combined Ratio of 67.3% and total underwriting margin of RM363 million.

Chart of GI Fire Combined Ratio Trend

Personal Accident Insurance

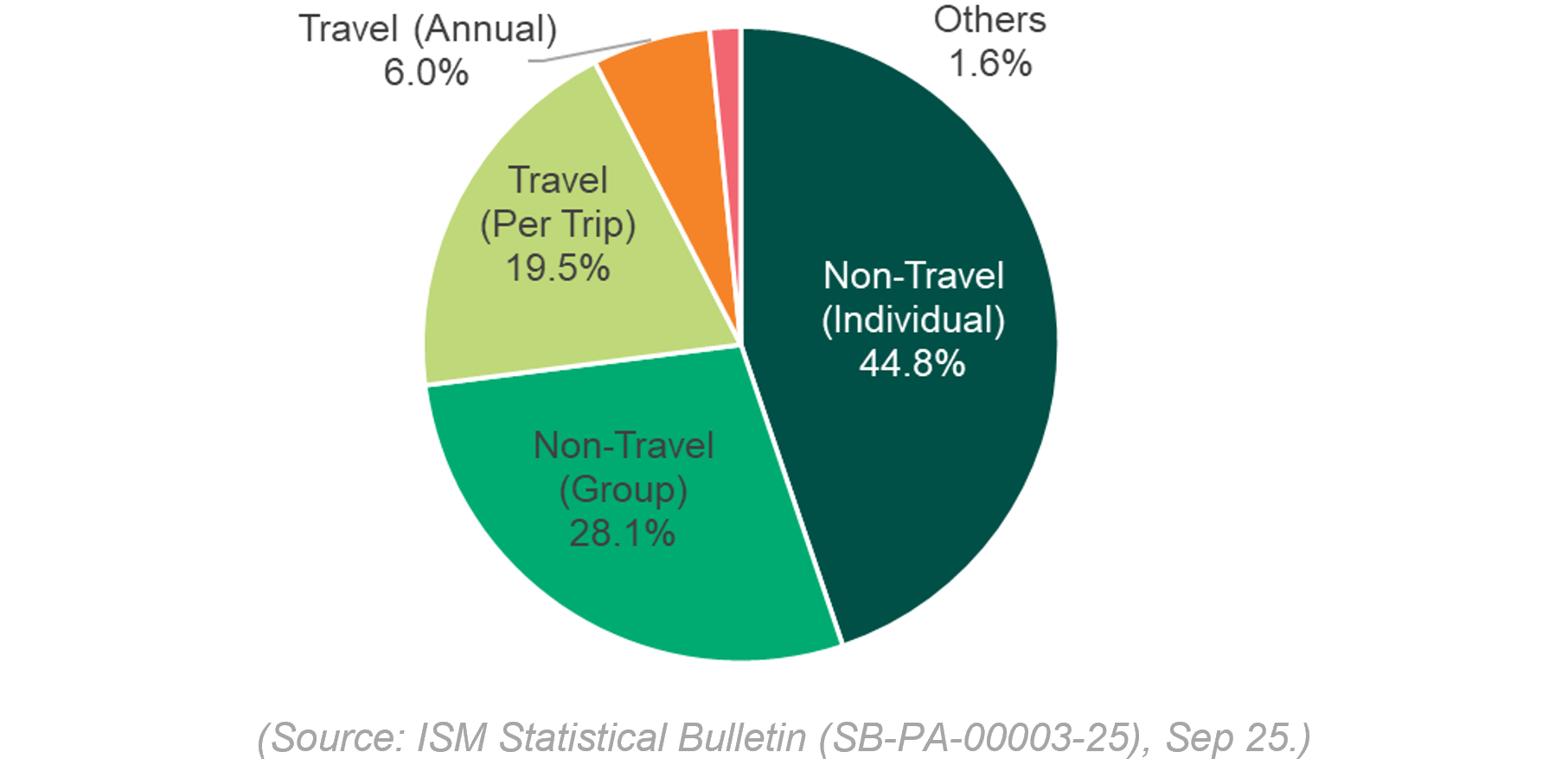

Personal Accident (PA) insurance also demonstrated strong growth, increasing by 11.2% to RM0.8 billion in GWP from RM0.7 billion in 1H2024. The growth for this segment was primarily from travel insurance.

Other Key Segments: CARE, and MAT

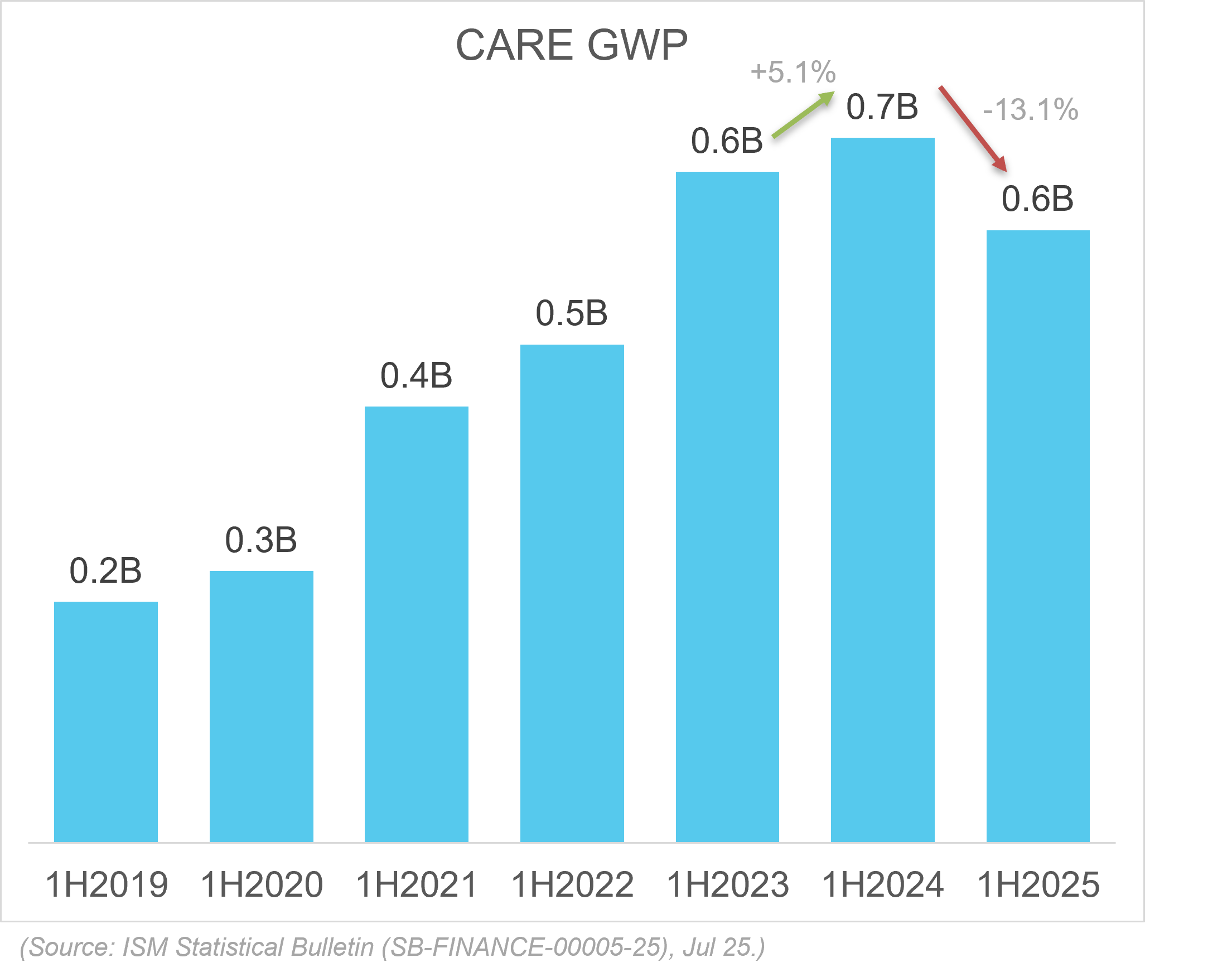

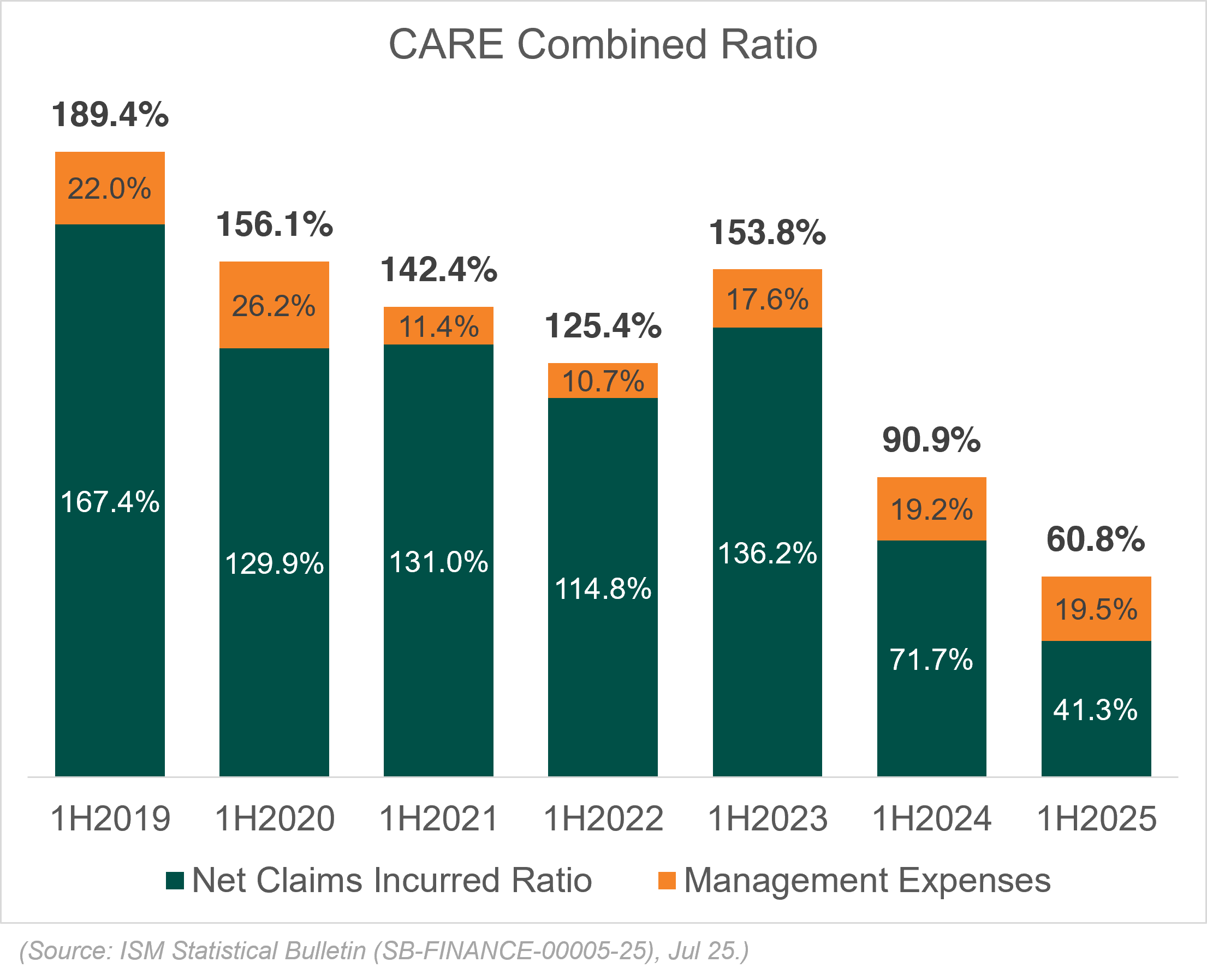

The Contractor’s All Risk & Engineering (CARE) segment recorded a 13.1% decline in GWP, falling from RM0.7billion to RM0.6 billion. Despite this contraction, the segment delivered a strong underwriting profit of RM58 million. This improvement was mainly driven by a sharp reduction in Net Claims Incurred Ratio (NCIR) which improved to 41.3% from 71.7% in 1H2024, likely reflecting fewer major projects.

Chart of GI CARE Combined Ratio Trend

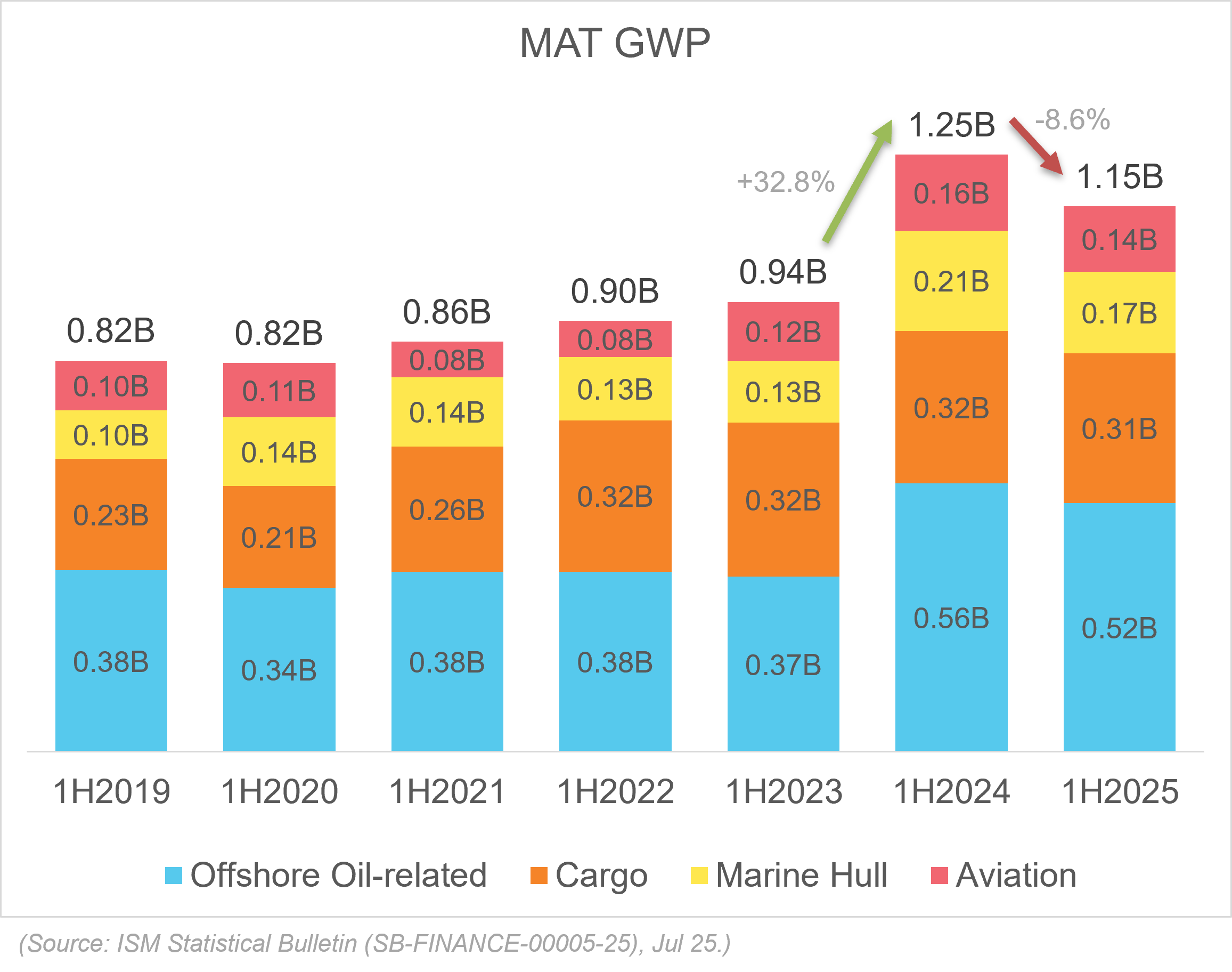

Marine, Aviation and Transit (MAT) insurance experienced a decrease of 8.6% from RM1.25 billion to RM1.15 billion in GWP. The Combined Ratio remained healthy at 63.2% in 1H2025 with an underwriting profit of RM76.9 million where Cargo and Marine Hull contributed 77.5%.

Chart of GI MAT GWP Trend by Classes

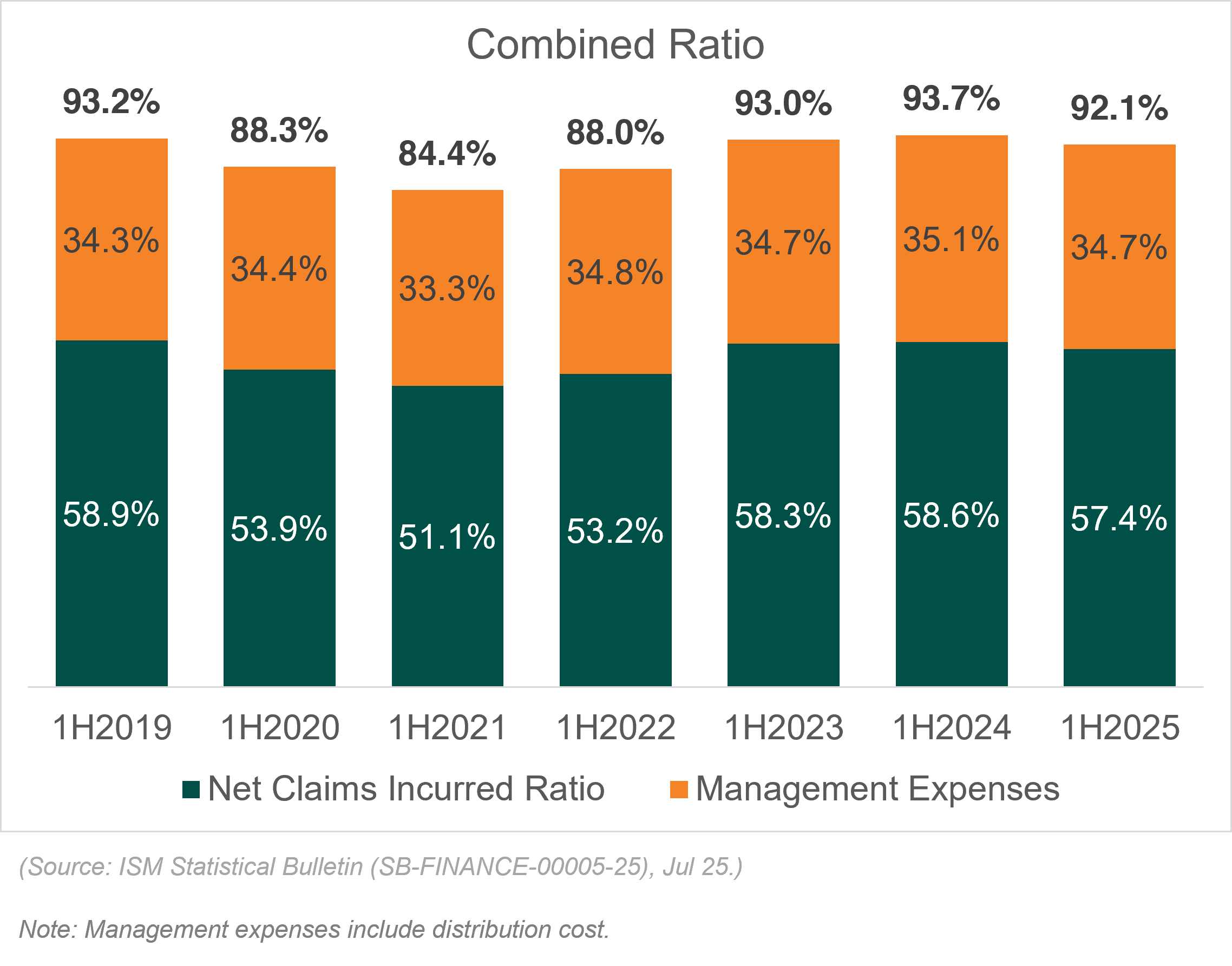

Performance Snapshot

The general insurance industry recorded an improved Combined Ratio of 1.6 points to 92.1% in 1H 2025 from 93.7% in 1H2024, indicating enhanced cost efficiency and maintaining stronger technical discipline and focus across key segments. The Net Claims Incurred Ratio (NCIR) slightly improved by -1.2 points to 57.4%, compared to 58.6% in 1H2024.

Chart of Overall Combined Ratio

Insurers will continue to focus on sustainable underwriting, operational efficiency, and innovation in product offerings particularly in electric vehicle (EV) coverage, climate risk solutions, and digital distribution channels to strengthen long-term resilience and competitiveness.

Navigating Headwinds

The industry continues to navigate a volatile external environment shaped by:

- Geopolitical uncertainty and trade impact e.g. US tariffs raised up to 19% on a wide range of goods;

- Intensifying climate-related risks and extreme weather events;

- Technological shifts, including cybersecurity threats, new technology risks and AI projects execution risk;

- Changing consumer demand with persistent knowledge gaps among consumers, coupled with rising expectations for faster and more accessible protection; and

- Economic pressures from high claims ratios, inflation, rising bodily injury claims, and escalating spare part costs.

These dynamics underscore the industry’s need to remain agile and committed to its dual mission: delivering a resilient, efficient insurance ecosystem while protecting Malaysian consumers.

Strengthening the Industry’s Role

To proactively address external demands and future risks, the industry is intensifying efforts across several strategic pillars:

-

Enhancing Financial Inclusion and Education

- Consumer Education Programme to empower consumers and enhance knowledge on financial protection

- Support of underserved segments where our members are actively participating in the Perlindungan Tenang Voucher (PTV) programme to strengthen essential protection for lower-income Malaysians, in collaboration with government stakeholders.

-

Talent Development & Innovation

- Promoting career development through the General Insurance Internship for Talent (GIIFT) programme, an industry-led 12-week on-the-job training initiative.

-

Road Safety

The industry is actively working with relevant stakeholders including enforcement authorities to enhance national road safety:-

Digitalisation of e-Police Reporting

The pilot e-Police Reporting was introduced on 1 September for minor accidents on the PLUS highway to expedite claims processing and response time. Since its launch,114 online reports have been lodged as at 3 October 2025. -

Research

Conducting research and engaging key stakeholders to strengthen preparedness and informed strategies to reduce road risks. Advancing EV insights to reduce emerging risks and strengthen the industry’s preparedness for this growing segment.

-

Digitalisation of e-Police Reporting

-

Flagship Road Safety Education Programme

-

PIAM will launch its free road safety education programme, “Langkah Bijak, Jalan Selamat” starting 2 November 2025. This programme is targeted at schoolchildren aged 10 and 11 studying in high-traffic zones like Brickfields, Kuala Lumpur focusing on teaching road safe road-crossing behaviours as they reach an independent age of commuting and/or mobility. Interested schools can contact corpcomms@piam.org.my to know more. Registration closes on 24 October 2025.

-